Closing the Generative AI Readiness Gap: What Telco Leaders Do Differently

March 2026

Altman Solon is the largest global TMT consulting firm with expertise in telecommunications consulting. In this insight, we share findings from our Generative AI Readiness Survey of over 100 senior telco executives worldwide.

Altman Solon is the largest global TMT consulting firm with expertise in telecommunications consulting. In this insight, we share findings from our Generative AI Readiness Survey of over 100 senior telco executives worldwide.

Generative AI is no longer just an efficiency tool or an IT experiment. For telecom operators, it is becoming an enterprise capability that reshapes how value is created, how capital is allocated, and how performance is managed. In Altman Solon’s 2025 Telco Generative AI Readiness Survey of 109 senior telecom executives, nearly three-quarters report measurable EBITDA uplift from generative AI initiatives. But the gains are uneven: leaders report approximately 7% uplift, while peers report around 2%.

That gap is not a rounding error. It is fast becoming a strategic fault line.

CEO reality check

-

When leaders are capturing EBITDA uplift, delaying action carries an opportunity cost. It's no longer whether to engage, but how to engage

-

A proliferation of AI pilots may signal enthusiasm, but without scale and value realization, experimentation can dilute focus and erode returns.

-

As AI systems become more autonomous and embedded in core processes, accountability evolves. Governance must be owned at the enterprise level and with isolated teams.

Across operators with similar resources, generative AI success is rarely defined by model quality alone. The difference is governance, capital discipline, operating-model design—and whether outcomes are owned by the business.

Our findings build on Altman Solon's earlier work on scaling generative AI in telecoms. Below are three insights that preview the report’s core findings, and why the next 12–18 months will separate leaders from followers.

Generative AI as an enterprise performance differentiator

In the telecommunications sector, generative AI is creating value across multiple domains at once, forcing trade-offs that no single function can resolve in isolation. In the survey, approximately 72% of realized value is concentrated in three domains: customer service, network operations, and marketing & sales, areas where cost, service quality, and growth decisions are tightly linked.

This concentration matters for two reasons:

First, generative AI is already producing measurable value, but only when it is operationalized.

Many operators can point to successful pilots. Far fewer can point to repeatable, scaled adoption with visible P&L impact. The organizations that scale treat generative AI as a business system: measured, governed, and embedded into day-to-day execution.

Second, the performance gap is widening because leaders govern differently.

High-performing operators distinguish themselves less by spending more, and more by how they make decisions:

-

Business leaders are on the hook for outcomes.

-

Generative AI is embedded into core operating models, not confined to IT or innovation.

-

A focused set of use cases is scaled with clear performance accountability.

This is why “generative AI failure” isn’t technical. It shows up as misaligned incentives, unclear decision rights, weak accountability, and fragmentation, especially when initiatives proliferate faster than the organization can absorb them.

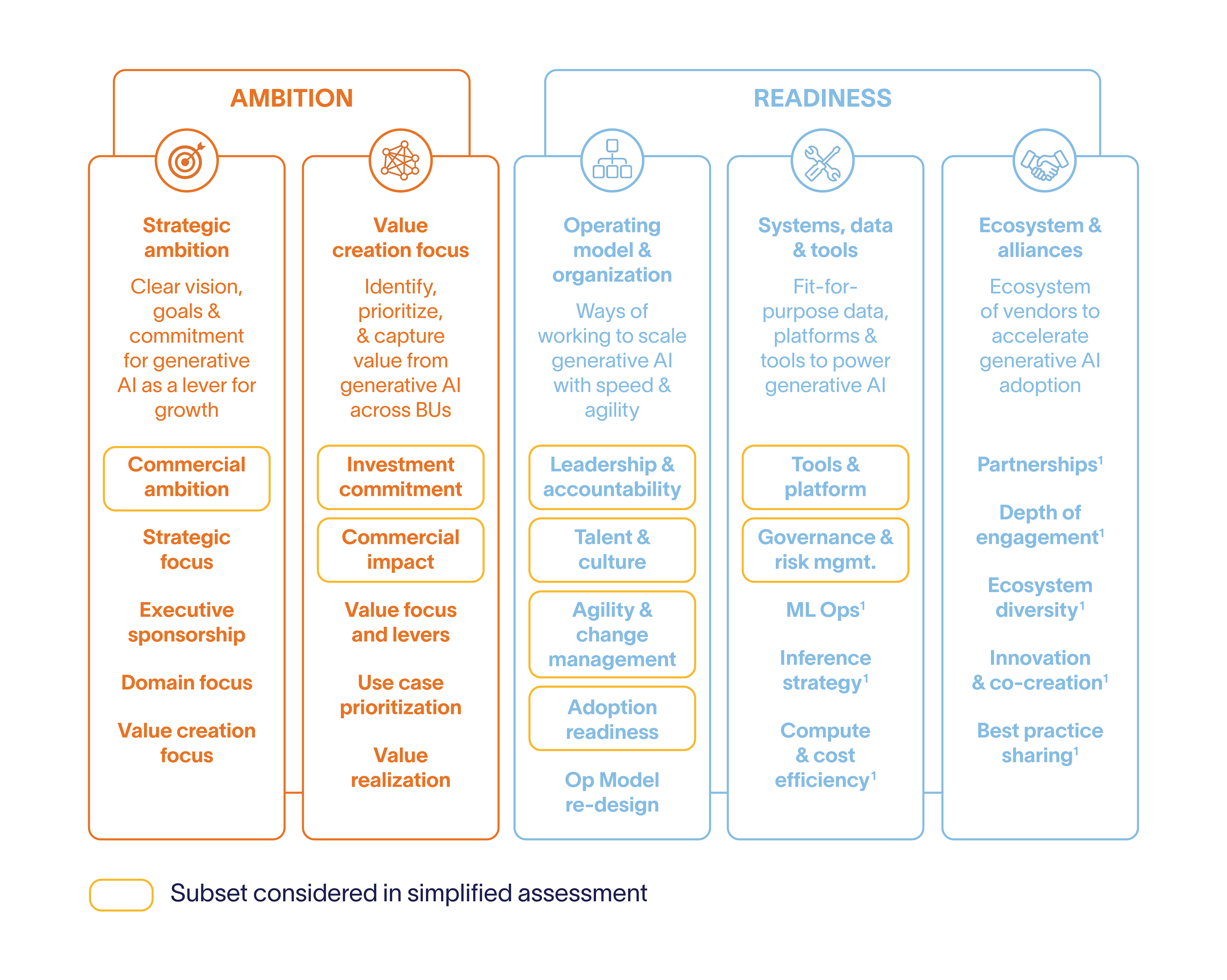

The ambition–readiness gap, why initiatives scale or stall

Ambition is high across telecom. Readiness is uneven, and that gap is now limiting outcomes.

A meaningful share of operators sits in a high-ambition, low-readiness position. They have bold targets and a large number of initiatives, but lack the alignment, governance, and embedded capabilities to deliver at scale. The pattern is familiar: dozens of projects, more than half stalling at the proof-of-concept stage, and a limited trace of impact on the P&L. The result is pilot congestion and ROI leakage.

On the other hand, roughly a quarter of operators show readiness exceeding ambition. These organizations have built strong technical and data foundations but remain cautious in deployment—held back by risk aversion, governance uncertainty, or leadership hesitation. In these cases, value is under-monetized: the capability exists, but the execution posture is too conservative to capture advantage.

Across both groups, one differentiator consistently explains performance:

Decision rights and accountability

Generative AI initiatives often involve multiple CXOs, but only about one in four operators reports full alignment between AI and commercial strategy. Execution improves not by adding more stakeholders, but by clarifying:

-

who can green-light scaling,

-

who owns downside risk,

-

and who approves autonomy thresholds.

High-performing operators decide faster, shut down underperforming use cases earlier, and scale with explicit P&L ownership.

In a constrained environment, leaders do fewer things better

Resource constraints are now a practical limiter of scale. Operators cite challenges such as talent shortages, integration complexity, and data/security/model-performance issues. The implication is straightforward: breadth becomes expensive quickly.

Leaders cap how many initiatives run at once and prioritize using three filters:

-

Feasibility: Can it be delivered with current capabilities?

-

Portability: Can it scale across functions or markets?

-

Expected ROI: Is the value meaningful enough to justify scarce capacity?

Use cases without clear portability are deprioritized by default. Combined with explicit stopping rules, this discipline concentrates scarce engineering and domain capacity where generative AI can move the needle most.

From efficiency to autonomy, what creates advantage next

Today, realized generative AI value is still predominantly efficiency-led. Many telcos focus investment on automation and near-term returns. But once scale is reached in high-volume, labor-intensive areas, autonomy becomes an economic necessity. Beyond certain volumes of tickets, faults, or campaigns, keeping humans in every loop adds cost and delay that erodes much of the value generative AI can create.

The question is no longer whether to deploy more autonomous workflows—it is how they will be governed.

This shift is already visible in network and operations. Many operators are deploying or planning capabilities such as self-healing networks, predictive maintenance, traffic optimization, and capacity planning, signaling that telcos are moving from assistive tools toward AI-driven execution. Operators leaning into more autonomous workflows report higher realized value per use case, especially where performance and reliability translate into financial outcomes.

But autonomy also shifts accountability away from individual users and toward the enterprise. That increases pressure to define decision rights, escalation paths, and financial controls. For many telcos, governance readiness, more than technology, is becoming the constraint.

A 12–18 month agenda for telco executives

Turning generative AI into a repeatable engine requires explicit choices, not more experimentation. Based on the research, five questions define whether generative AI becomes self-reinforcing—or remains a collection of stalled pilots:

-

Which top three generative AI use cases will carry explicit P&L ownership?

-

What autonomy thresholds will we allow in network operations and customer care?

-

Which initiatives will we stop funding in the next 6–12 months?

-

How will realized value be reinvested—and who has decision rights over reinvestment?

-

What operating-model changes are needed to scale generative AI safely and repeatably?

Executives who answer these questions clearly and act on them move generative AI out of pilot mode and into the core business, embedding it into decision-making, performance management, and capital allocation. Those who defer them may keep ambition high while value remains fragmented.

How Altman Solon can help with generative AI readiness

Altman Solon helps telecom operators move from generative AI ambition to measurable business impact, by clarifying where value sits, what to scale first, and how to govern it.

-

Assess readiness and value at stake. Benchmark ambition and enterprise readiness, identify the biggest gaps, and size priority value pools.

-

Prioritize and scale the right use cases. Build a focused portfolio with clear stopping rules, defined owners, and KPIs tied to the P&L.

-

Design the operating model for autonomy. Establish decision rights, risk controls, and execution paths that support scaling, especially as use cases become more agentic.

Get the full findings from Altman Solon’s Telco Generative AI Readiness Survey and see how leading operators are governing, prioritizing, and scaling generative AI for measurable outcomes.

Related topics

Read the full whitepaper

Insights

Insights | August 2026

Insights | July 2026

Insights | July 2026