How Sports and Streamers Can Help Latin American Pay TV Retain Customers

July 2021

The COVID-19 pandemic has accelerated the global streaming trend, with the launch of dozens of new streaming services, including many popular options throughout Latin America, over the past year. In the region, this explosion of streaming options has led to more “cord cutting,” or the canceling of traditional pay TV subscriptions in favor of Internet-based services, which are often cheaper and more customizable. Furthermore, even newer Over-the-Top (OTT) options, including Virtual Multichannel Video Programming Distributors (vMVPD) and ad-based Video-on-Demand (VOD), are further crowding the Latin American TV landscape.

While these new competitors create challenges for Latin American pay TV providers, there are unique dynamics in the regional markets that help providers retain customers and provide opportunities to deliver programming – like live sports and news – that many viewers cannot access elsewhere. Still, pay TV providers must act quickly and decisively to capitalize on these natural advantages – such as providing access to millions of consumers without credit cards – and forge new partnerships with the same streaming services that they compete with for viewers.

Latam viewers hungry for sports & news

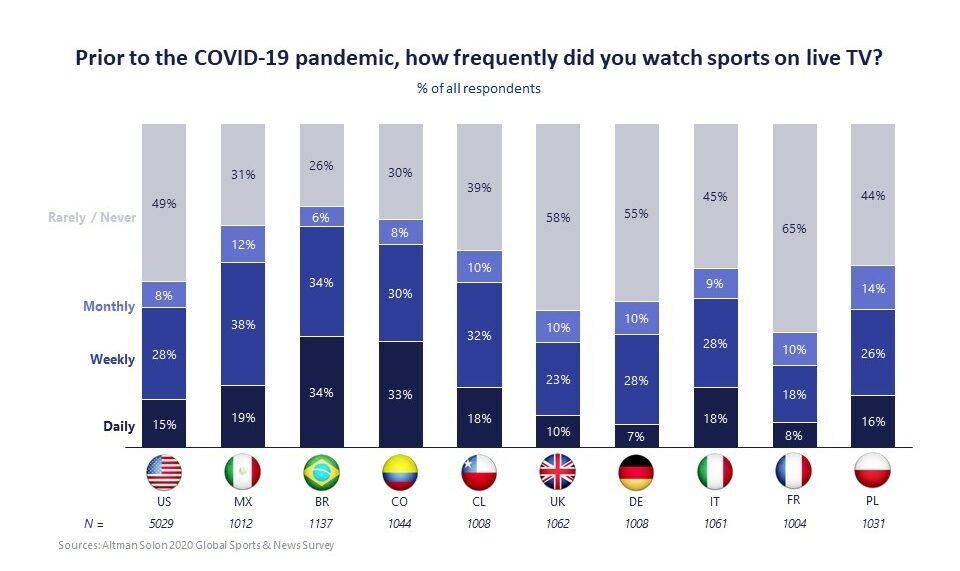

While it is not a surprise that Latin American TV viewers love watching football, data from Altman Solon’s Global Sports & News Survey shows just how important live sports – along with live news – have become to pay TV subscribership in the region. The survey found that Latin American countries (Brazil, Chile, Colombia, Mexico) have among the largest differences in pay TV subscription rates between sports and news viewers and those who don’t watch sports and news regularly. In Brazil, regular sports and news viewers subscribe to pay TV at an 82% higher rate than non-sports and news viewers, the largest delta of any country tested. Sports and news viewers in Mexico (45%) and Chile (47%) also subscribed to pay TV at a much higher rate than non-sports and news fans.

With the proliferation of streaming services and mobile viewing, scant traditional “appointment viewing” remains. The days of millions of viewers tuning into a popular drama or sitcom at the scheduled time have given way to binge-watching on streaming services and recording shows to watch later.

News and sports, however, are content that viewers still want to watch in real-time. That reality has been reinforced during the pandemic as viewers look to keep current on news developments related to COVID-19. In fact, the survey found the largest surges in news and sports interest in Latin American countries. In Chile, for example, 36% of viewers say they watched an additional six or more hours of live news since the start of the pandemic, the largest increase of the countries surveyed. This is not just a pandemic bump: the survey revealed that Latam viewers watched sports more regularly – and for longer durations – than those in Europe and the U.S. prior to COVID-19.

Latam Pay TV pricing structure: lower risk of cord cutting vs U.S.

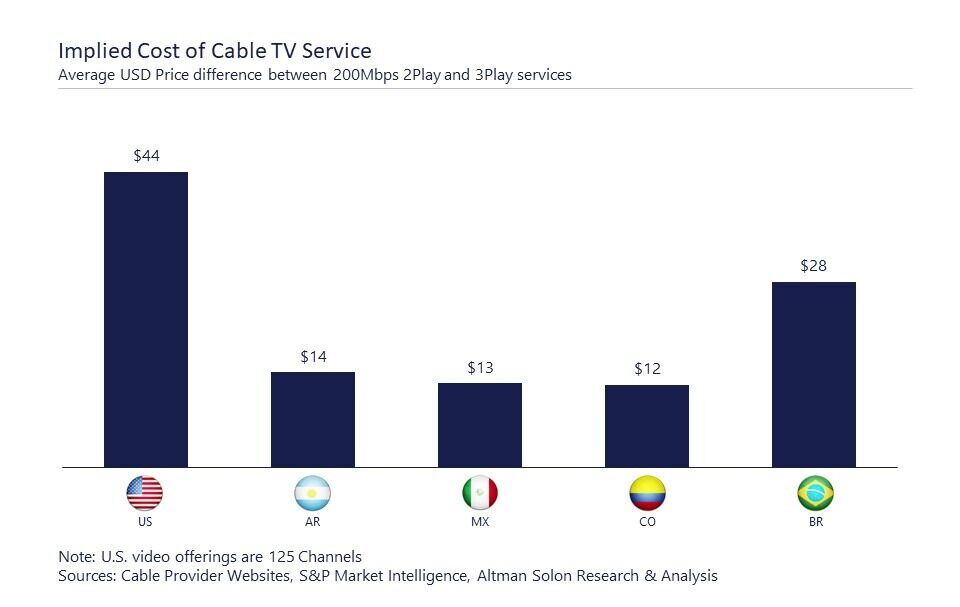

The trend of cord-cutting has existed for more than a decade but has accelerated as some consumers discontinue pay TV in favor of relying primarily on accessing streaming content through internet-only services – including Subscription-Based, Advertising-Based, and Free OTT platforms. The decision to discontinue Cable TV is in large part motivated by cost. For example, in the U.S., the implied cost of pay TV (estimated as the cost differential between triple play and voice plus internet double play packages) ranges between $40-90 depending on the number of channels and other features.

Notwithstanding the relative income differences among different countries, the implied cost of subscribing to pay TV services in Latam is substantially lower than in the U.S. For example, in Mexico, Colombia, and Argentina, the implied cost of pay TV ranges between $12-$14. In Brazil, the implied pay TV cost is just under $30.

These differences in the cost of pay TV can have a significant impact on how Latam consumers assess the trade-off between traditional pay TV and OTT services. The savings realized by cancelling traditional pay TV service in Latam would only cover a single OTT subscription (for example, a monthly Netflix subscription in Mexico costs up to $13), at the expense of foregoing dozens of TV channels, including live events. Such trade-offs make canceling pay TV in Latam much less attractive than in the U.S., especially for viewers who value live TV, including popular news and sports programs.

Latam credit card penetration: no credit card, no problem

Another factor on the side of traditional pay TV providers is the low penetration of credit cards throughout Latin America. In most Latin American countries, fewer than one-third of consumers have an active credit card, and in Mexico, Colombia, and Peru, that rate plunges to 20% or less. Latin America’s northern neighbors, by contrast, have much higher rates: the United States has 65% credit card penetration, while nearly 80% of Canadian adults have at least one credit card, per a 2020 World Bank study.

Since credit cards are the primary payment method for streaming services and vMVPDs, the limited credit card penetration essentially eliminates 70% or more of consumers in most markets for subscriber-based streaming platforms. As a result, pay TV providers enjoy a natural advantage in Latin America by having the billing and collections mechanisms in place for millions of subscribers (e.g., physical points of presence, bank, and retail payment network partnerships). In essence, pay TV providers are a critical avenue for reliable billing and collections to millions of households in Latam countries with massive under-banked populations.

Streaming partnerships: win, win…win?

The lack of credit cards has forced streaming providers to develop platform-sharing agreements with incumbent pay TV providers to reach these non-credit cardholders and other consumers. With these new partnerships, which are typically offered by cable companies as TV-Internet-Phone bundles with streaming subscriptions included, OTT platforms like Amazon Prime and Netflix can connect with non-credit card viewers – as well as other customers loyal to traditional pay TV providers – without changing their payment models or investing in targeted marketing.

The recent big launch of HBO Max Latin America, which is now available in 39 Latam and Caribbean markets, illustrates the strategy of streamers partnering with pay TV providers. HBO Max’s aggressive promotional deals (50% lifetime discount for new subscribers who sign up before the end of July) and focus on popular specialized content, including football (UEFA Champions League for Brazil and Mexico), will help build the regional subscription base, forging partnerships with pay TV providers throughout Latam may be more important to the streaming service’s long-term success. HBO Max has already partnered with major Latam providers, including DirecTV, Megacable, America Movil, and Sky, in addition to providing customers of regional providers with existing subscriptions to HBO through Claro Video (Mexico), Claro (Brazil), Oi (Brazil), Tim (Brazil), Totalplay (Mexico), Vivo (Brazil), and VTR (Chile) with access to HBO Max free of charge.

This week, ViacomCBS Networks International announced a deal to deliver its Paramount Plus streaming service to Tigo’s pay TV customers in Bolivia, Costa Rica, and Honduras. Tigo plans to extend this arrangement to its mobile customers soon.

For pay TV providers, partnering with streamers helps mitigate cord-cutting, which has been the scourge of pay TV companies for the past decade. With access to the popular content on streaming services, along with the stability and comfort of cable services, there is little incentive for consumers to cut the cord. These partnerships, at least in Latin America, are a rare win-win for direct competitors in the media space.

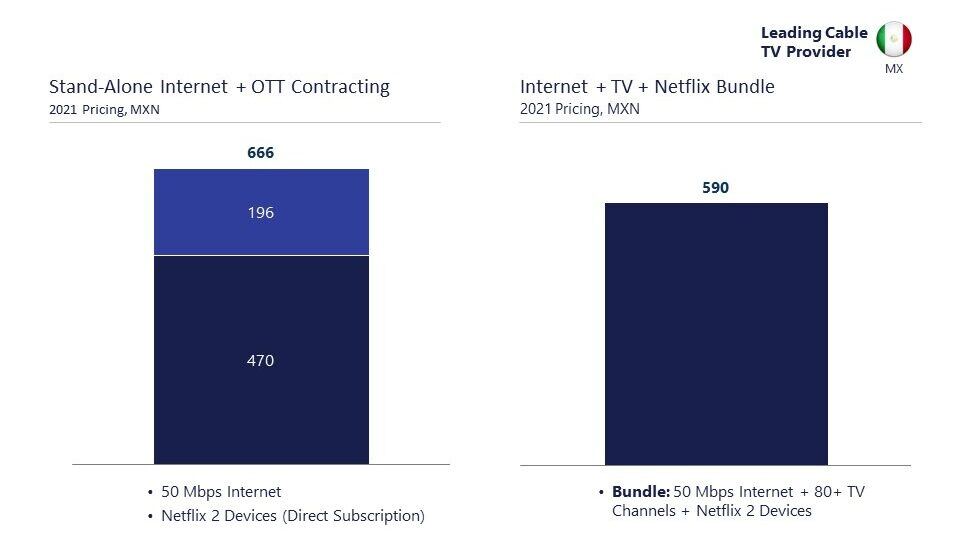

And, it turns out, the consumer wins too: the average cost of bundles offered by pay TV providers that include high-speed internet, pay TV service, and major streaming service subscription (e.g. Netflix) is more economical than stand-alone internet service and a streaming subscription – without any pay TV service (see below example for Mexico).

Cost is one of the primary reasons that viewers choose to cut the cord. Offering competitively priced bundles that also deliver the content they crave effectively removes cost as an issue. In fact, these bundles provide more services and content – including coveted live sports – for a similar price. With cost removed, there is little incentive for consumers to make a potentially disruptive change by moving to a relatively unproven new TV service. In the long run, these bundles – if priced right – will strengthen customer loyalty and help pay TV providers find the Holy Grail: a way to slow cord cutting.

Insights