Tech-Savvy Daily “Super Shoppers” Push E-Commerce Merchants to up Their Game

May 2022

Altman Solon’s global TMT strategy consulting leadership team brings both advisory and operational experience across the supply chain landscape when consulting with e-commerce merchants, supply chain partners, and global corporations. The firm’s digital commerce experience spans industries and continents, advising on sales effectiveness and efficiency, market sizing and trends, retail warehouse opportunities, commercial due diligence, and operational strategies for cost reduction, among others.

How boosting speed, flexibility, and community in Direct-to-Consumer supply chains can meet the demands of the modern shopper

E-commerce has existed since the 1970s but began its mainstream rise in 1992 with the launch of Bookstacks Unlimited, one of the first online marketplaces accessible to the general public. Thirty years later, the technology and logistics of online shopping have become more sophisticated, and the consumers have as well.

Altman Solon’s 2022 Consumer Supply Chain Fulfillment Survey reveals an online shopping public – particularly a subgroup of daily “Super Shoppers” – that prioritizes speed, flexibility, and community over price. The survey, which polled over 1,300 U.S. consumers in February, also reveals strategies for how Direct-to-Consumer (DTC) providers can optimize the design and operations of their supply chain and implement more effective e-commerce strategies.

Rapid growth for fast delivery

E-commerce has grown significantly over the past few decades and is now unrecognizable from the humble beginnings of Bookstacks Unlimited. According to eMarketer, retail e-commerce sales in 2021 reached $4.9 trillion worldwide and are projected to grow to approximately $7.4 trillion by 2025.

Within the sector, certain subsets have experienced even more robust growth. Online grocery sales – driven by startups like Instacart and apps from retail giants like Walmart+ and Amazon Fresh – grew by 54% in 2020 as COVID-19 restrictions made in-person shopping more difficult. Ultra-fast delivery – defined as delivering goods within a 10–15-minute window – skyrocketed by 346% in the U.S. in 2020. This retail growth comes as investors – including those from the U.S., the U.K., and Spain – are putting more money into ultra-fast providers.

Still, there are signs that growth in the ultra-fast sector has its limits: in March, two high-profile ultra-fast delivery startups, Fridge No More in New York City and Byuk, which operated in Chicago and New York City, shut down over financing issues.

Delivery: Make it fast

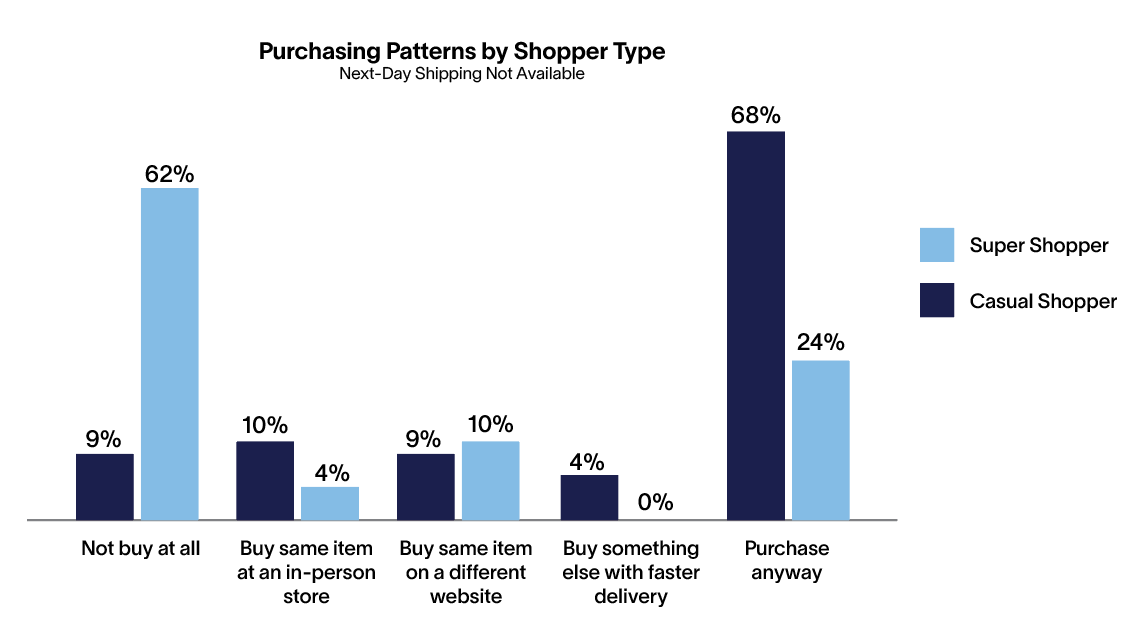

The ultra-fast movement has been driven by newer companies like Instacart and GoPuff but started with Amazon establishing two-day shipping as an industry standard across a number of verticals. Consumers have developed the expectation that most goods can be delivered quickly, and, according to the survey, many are willing to pay for speed. The survey reveals that next-day delivery is a key purchasing criterion for a large population of shoppers – particularly for Super Shoppers – those making purchases daily or more frequently – 62% of whom say they will “not buy a product at all” if they cannot get it delivered the next day or sooner.

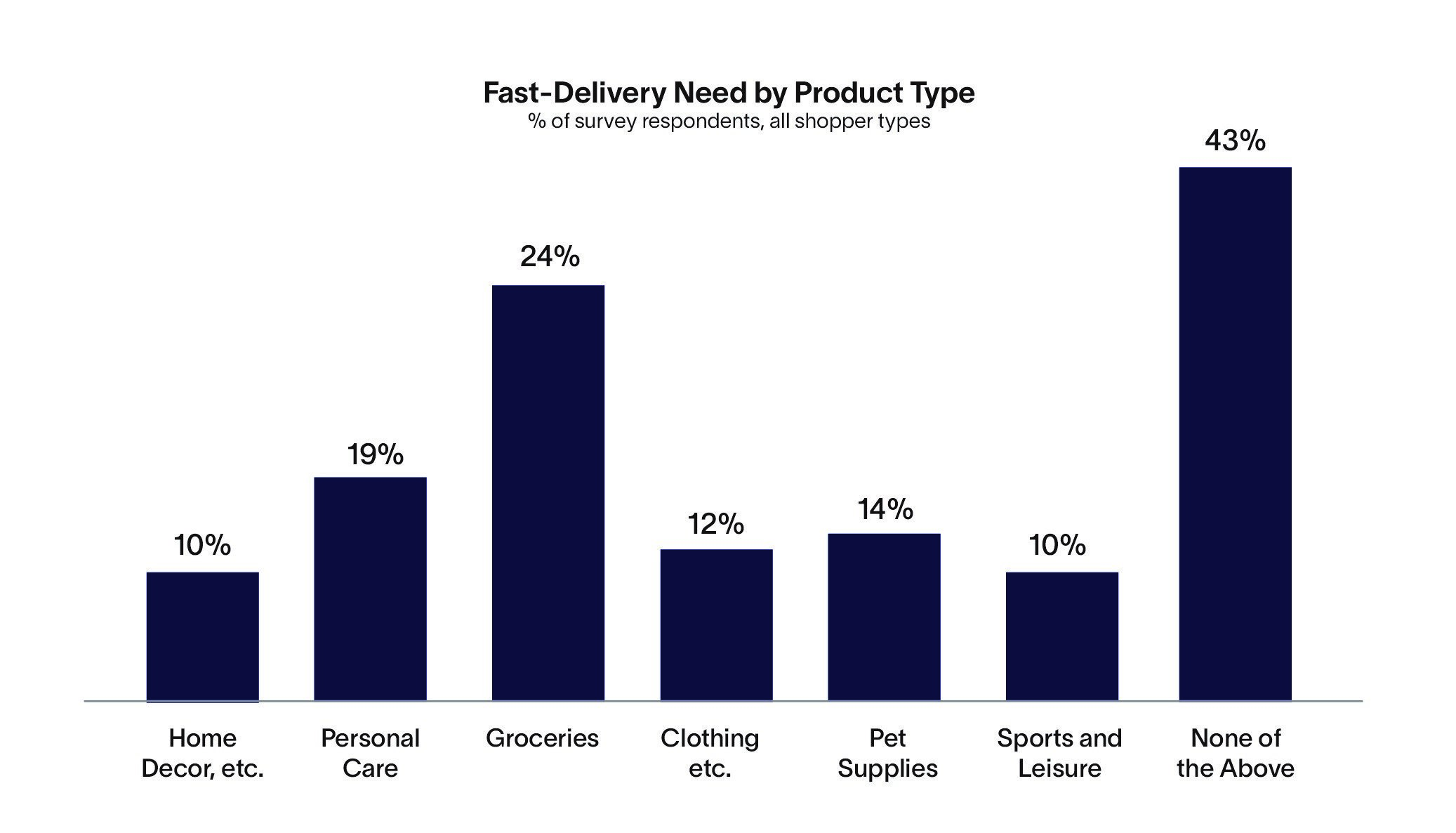

For all online shoppers making purchases at least monthly, exhaustible or perishable products, including groceries, personal care products, and pet supplies, rank highest in fast-delivery priorities. Online shoppers view reusable or less than daily-use products like sporting goods, clothing, and home décor products as less important to receive quickly.

Staying on tracking

In recent years, keeping tabs on shipping orders has become easier for consumers as retailers have tapped into better tracking services from FedEx, UPS, and the U.S. Postal Service. Retailers have also adopted new tracking functions, like photos of the packages arriving at consumers’ doors and real-time location tracking.

The survey shows that many consumers are taking advantage of tracking services. Nearly two-thirds of online shoppers track packages more than half of the time they place an order.

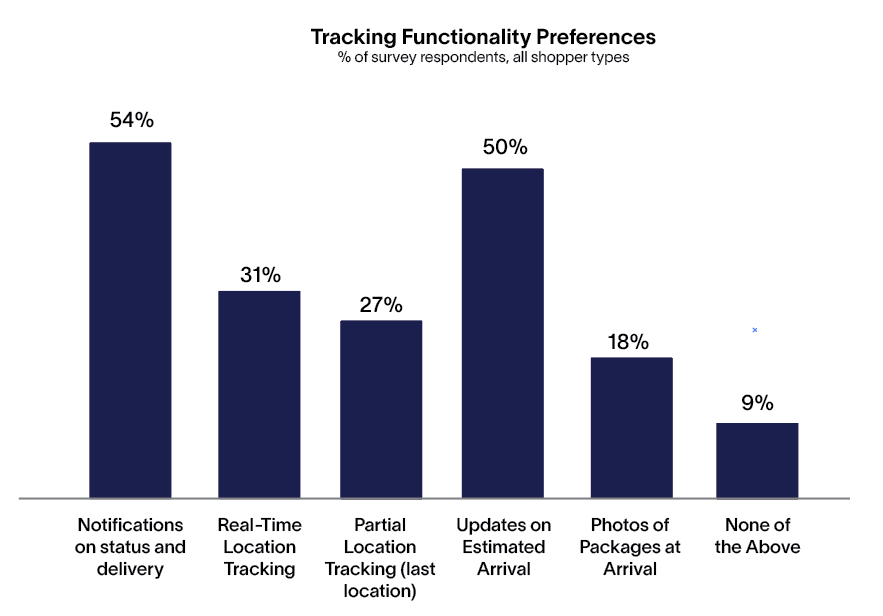

The survey noted that, at least so far, most consumers are uninterested in (or unfamiliar with) using newer functions like porch photos or real-time tracking. Instead, a majority of consumers say they prefer more established tracking functions, like delivery/status notifications and estimated arrival updates.

Return to sender

Returns have never been a favorite activity of consumers, a view that is reinforced by the survey results: 31% of Casual Shoppers, those making purchases on a weekly or monthly basis, identify returns as the biggest pain point. But doing returns right is critical for online retailers to establish trust with consumers. While returns in certain ways have gotten easier, shoppers who don’t own a home printer (and are in the office less due to COVID-19) often struggle with printing the shipping labels needed for returns. Super Shoppers in the survey pointed to more difficulty printing return labels than their Casual Shopper counterparts.

Survey findings suggest more time to return unwanted items is a top preference across all shopper segments: 31% of Casual Shoppers and 22% of Super Shoppers noted time to return as the largest pain point.

“When it absolutely, positively has to be there overnight,”…consumers will pay

In the 1970s, FedEx introduced the above slogan, revolutionizing shipping by offering next-day delivery. For decades, overnight delivery was mainly for important business documents but was not a focus of e-commerce. Through overnight delivery of certain items, Amazon helped change consumer culture and entrenched next-day delivery as an industry standard.

Consumers, particularly those who make frequent online purchases, are willing to pay: 80% of Super Shoppers say they are willing to pay for next-day delivery, including 35% who will pay $20 for that service. By comparison, a majority of Casual Shoppers refuse to pay for next-day delivery, and only 4% will pay $20.

What it means for investors

There has been a recent flurry of merger and acquisition activity and increased VC/PE investment in delivery companies, but what does that mean for the future of the sector? For every success, like GoPuff, Instacart, and ShipBob, other companies, like Byuk and Ship No More, do not make it.

The survey reveals specific ways that investing across different variables for delivery/returns can drive value for the consumer. Large supply chain providers like Amazon and Walmart are finding themselves competing with smaller, more nimble players who are developing alternative solutions to meet the changing needs of e-retailers and their customers. A few areas where successful investments have been made include:

- Technology companies developing end-to-end platforms that integrate supply chain capabilities and emerging technologies (i.e., predictive/AI analytics, cognitive technologies) to drive efficiencies, untapped revenue opportunities, and customer insights for both outbound deliveries and reverse logistics.

- E-commerce companies partner with warehousing and freight logistics companies to react quickly to rapidly changing consumer preferences and attitudes across varying ordering sizes, frequencies, and products.

- Supply chain companies that are extending the supply chain capabilities of small- and medium-sized merchants on a global scale by leveraging core technologies and partnerships.

What it means for e-commerce merchants and supply chain partners

In the past few years, through the pandemic and the war in Ukraine, the global supply chain has gotten more attention than ever before. While most of the doomsday scenarios predicted in the media didn’t come to pass, consumers have experienced some product scarcities and long delays for bigger items like cars and furniture.

The survey data is revealing about the online shopping habits of the modern consumer, but what does it mean for e-commerce merchants, supply chain partners, and others with responsibilities along the supply chain? An agile supply chain is crucial for success in meeting rising consumer demands within the e-commerce market, and developing an agile supply chain requires retailers to invest in new supply chain innovations and strategic partnerships. But, with all of the new solutions available for retailers, which strategies provide the best return on investment?

Altman Solon’s survey analysis points to creating a strategy that focuses on the most active and sophisticated consumers: the Super Shoppers. To do that, retailers should prioritize investments to make that segment happy through a better customer experience (CX), while fostering lines of communications with Super Shoppers. Here are some ways to do that:

- Boost at-home returns – Returns are a proven pain point for all consumers, but Super Shoppers, with their higher frequency of orders and returns, are especially picky about returns and are engaged enough to seek retailers that do it well. While Super Shoppers will appreciate return reforms like extended return windows or providing hard copy return labels, they hope to skip the trip to the post office or UPS store. While the survey shows overall modest early interest in at-home returns, Super Shoppers chose at-home returns at twice the rate of Casual Shoppers. Stronger promotion of at-home returns could push more Super Shoppers to the retailers that make returns nearly pain-free.

- Create subscriptions for next-day delivery—Similar to how Amazon popularized free delivery through Amazon Prime, retailers could create a subscription service for next-day delivery to attract and retain Super Shoppers. Given Super Shoppers’ penchant for fast delivery, this monthly fee-based subscription service would generate new revenues and reduce the number of missed sales due to slower delivery. In addition, it would help create a sense of community for Super Shoppers who appreciate the exclusive service.

- …And build on that sense of community – Super Shoppers demand a better CX but also appreciate retailers that value their opinions. Retailers should regularly pulse frequent customers to ensure the Super Shoppers’ high standards are being met – and even to solicit opinions on how to improve service. Retailers could also engage Super Shoppers through social media and create exclusive digital forums to connect their best customers with each other.

While it is not a new strategy for retailers to cater to their best customers, the fact that Super Shoppers aren’t walking into a brick-and-mortar store every day requires different strategies to improve CX and build and maintain customer loyalty. The survey shows that making an investment in Super Shoppers is the right strategy at this point in the e-commerce evolution – and reducing prices is much lower on the list than other high-touch reforms.

From December 2021 to January 2022, Altman Solon ran two consumer surveys to understand preferences around delivery speeds, tracking functionalities, and return processes and glean insight into e-commerce supply chain capabilities. Through survey analysis, the respondents were segmented by shopping frequency, defining a Super Shopper segment – those making purchases daily or more frequently – and a Casual Shopper segment – those shopping weekly or monthly. Nearly 720 consumers participated in the survey specific to returns, and 600 consumers responded to the delivery and fulfillment survey. All survey respondents were from the United States.

Insights