INSIGHTS

The negative macroeconomic effects of COVID-19 have been swift and unprecedented. The job losses, driven in large part by massive cuts across retail, travel, and hospitality sectors, have been historically bad, but the economic fallout has been overshadowed by the public health costs: in recent weeks the U.S. surpassed the grim milestone of more than 100,000 dead due to COVID-19.

As some regions are starting to lift stay at home and work restrictions, there is hope, buoyed by some early evidence, for a potential bounce back due to pent up demand and a surprisingly resilient (if volatile) stock market. In April, Altman Solon explored how the COVID-19 pandemic will affect Telecom, Media, and Technology (TMT), the sectors we cover. This piece focuses on the impact of COVID-19 on B2B wireline and cloud services by using available economic data to create our own growth projections for key market segments: voice (traditional and IP voice services), business internet (dedicated internet access and standard broadband), networking (enterprise WAN and VPN services), wholesale (backhaul for towers, front haul for small cells, and wholesale transport and IP transit) and cloud (IaaS) services. Our forecast is also built up by customer segment, forecasting impact on small to mid-size business (SMB, locations with fewer than 50 employees) vs. Mid-Market (50-999 employees) vs. Enterprise (1,000+ employees) vs. Carrier spend.

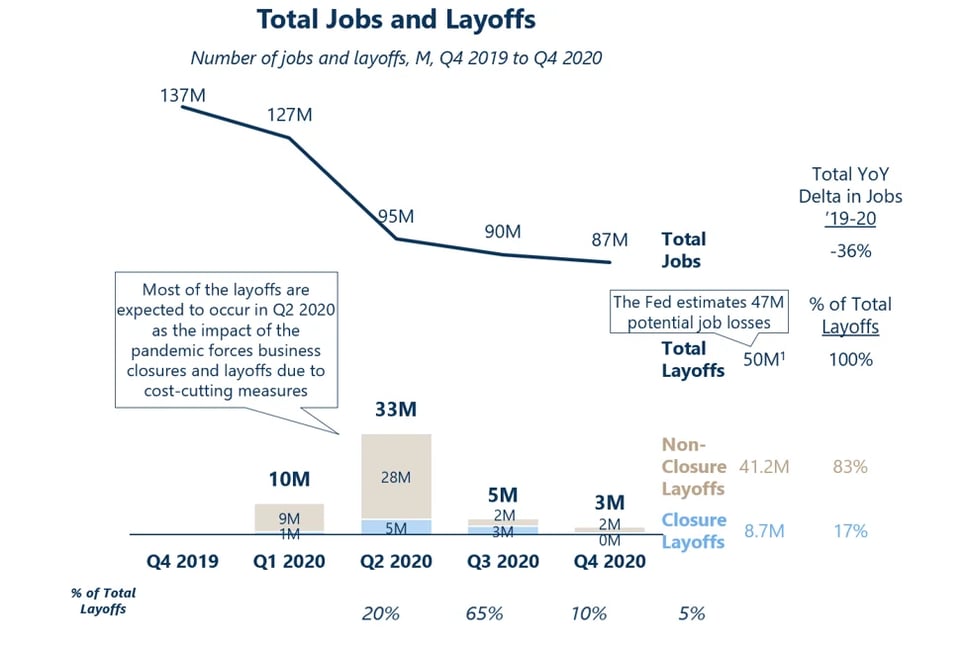

The basis for our market forecast assumes that the U.S. will lose 50 million jobs (-36%) from COVID-19 in 2020, with four out of five of those cuts coming from layoffs. The remainder of lost jobs will come through business closures, nearly all of which will be SMBs.

While recently released economic reports suggest COVID-19 has cost the US between 20 million and 40 million jobs thus far this year (through May), which is below our assumed 50M, it’s unlikely we have seen the full impact of COVID-19 on the economy yet. Any lingering slowdown in consumer demand or re-introduction of stricter social distancing measures if death counts spikes up again are likely to result in more job losses by year’s end.

Still, our projections reveal hopeful trends for telecom despite the current economic conditions; in fact, some segments are already seeing demand and sales increases because of the current conditions. The global supply chain for telecom is robust and diversified and has held up relatively well to this environment, with providers continuing to serve current demand and move nimbly to address future customer needs.

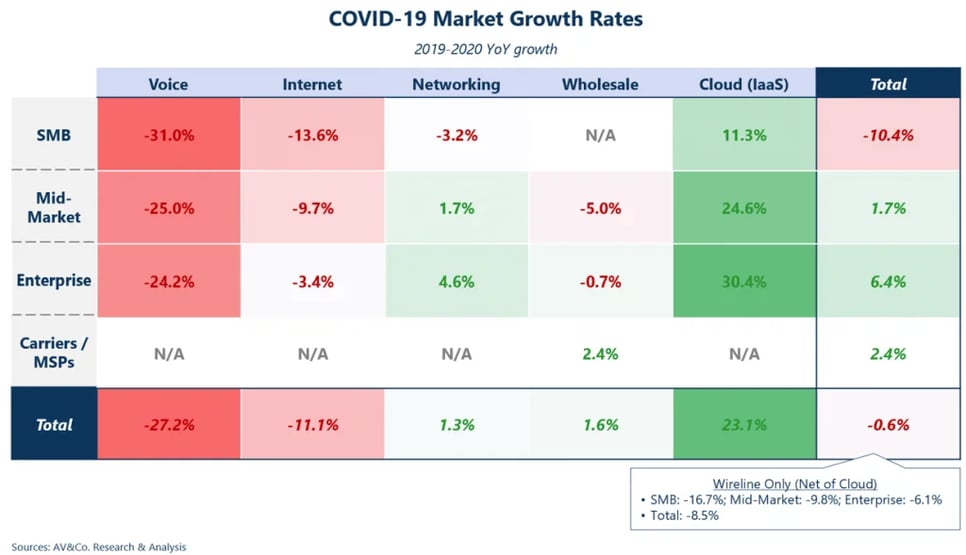

In the short term (2020) there is some good news, particularly for cloud providers. Although certain traditional B2B wireline products, like voice, will be hit hard, most of the others will still experience growth. The overall sector will only see a nominal decline of -0.6% year-over-year in 2020, though it is buoyed by a large and still rapidly growing cloud market. Removing the cloud market, the B2B wireline products will see a decline of -8.5% year-over-year.

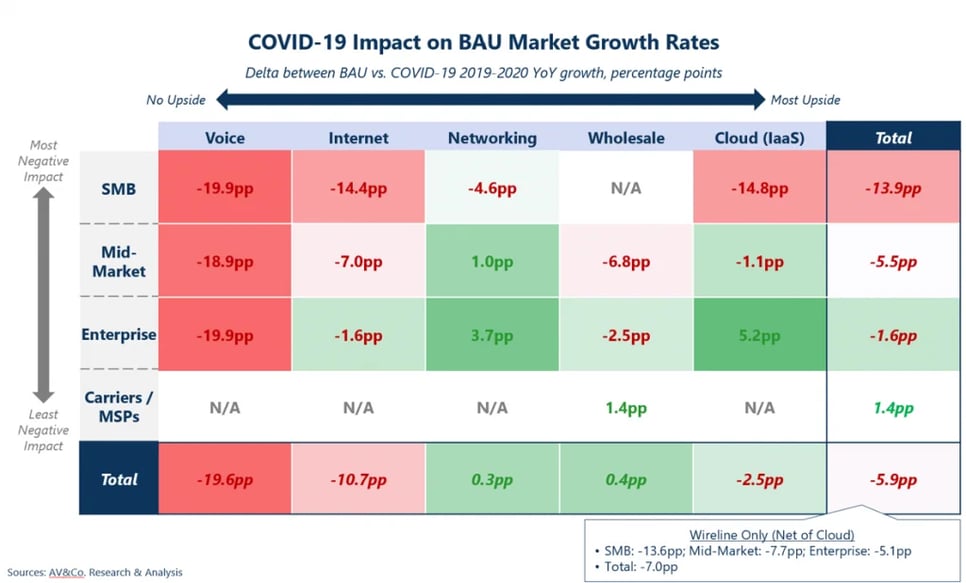

Of course, this modest growth is a far cry from where our analysis says these markets would be had COVID-19 never struck. Our analysis shows that COVID-19 is causing a -5.9 percentage point impact on the overall growth trajectory, meaning a Business-as-Usual (BAU) scenario would have seen the sector increase a healthy 5.3 instead of decline nominally by -0.6%.

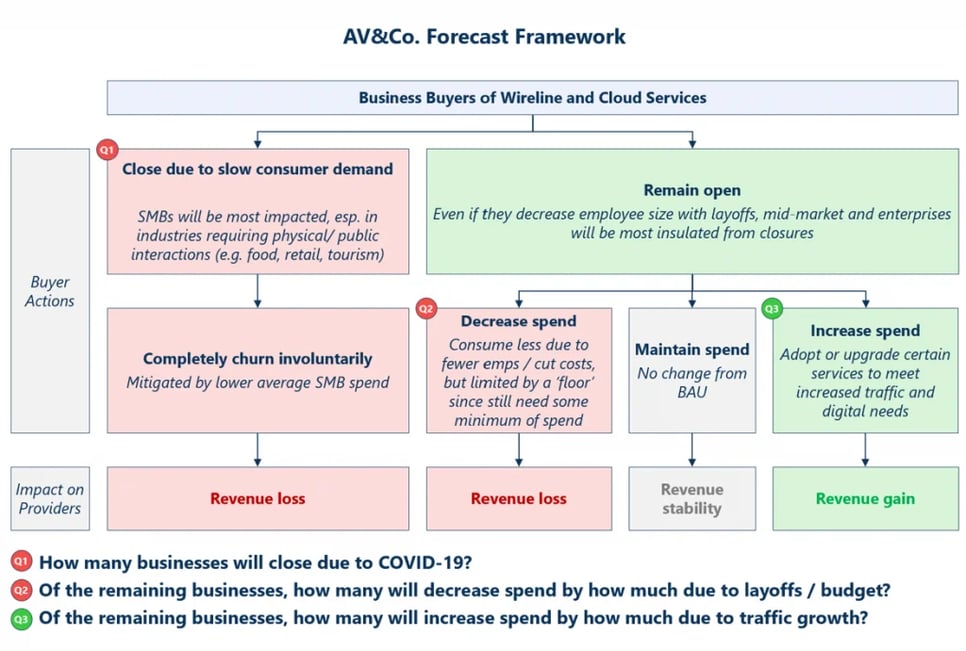

We forecasted COVID-19’s impact based on underlying demand drivers for each of the products we analyzed. This is a unique economic downturn, in that while the overwhelming impact on the economy will be negative due to the ongoing business closures and layoffs, some B2B wireline and cloud products will see an offsetting increase in demand as they are playing an increasingly critical role in enabling the new “remote” workforce. Given this, we aimed to answer, for each of the products we analyzed, three key questions:

- How will the business closures impact the addressable customer base for this product?

- How many of the remaining businesses will decrease spending, and by how much, due to layoffs or budget constraints?

- How many of the remaining businesses will increase spending, and by how much, due to traffic and/or usage growth?

The results show a mixed short-term outlook for nearly all B2B wireline and cloud products. Market sectors with greater exposure to SMB will see strong headwinds from COVID-19, while products that play a larger role in enabling remote work and more distributed network access (e.g., VPN, Cloud) experience offsetting tailwinds.

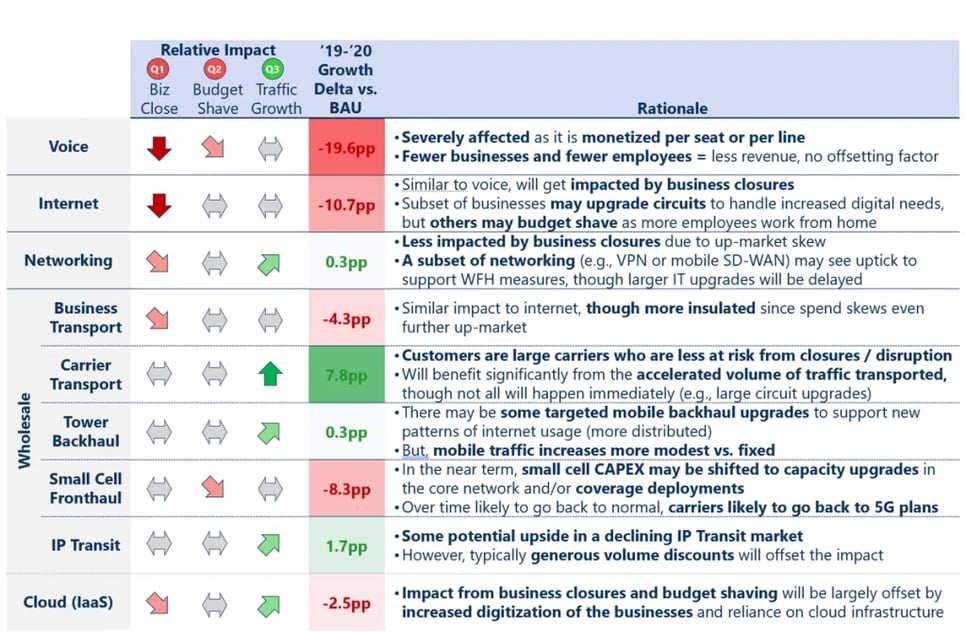

Voice (Traditional and VoIP)

Voice (Traditional and VoIP) will be hit hardest by COVID-19 in terms of 2020 business closures given over-exposure to the SMB segment, which faces the most near-term economic risk. In addition to business closures, layoffs at surviving businesses will also lead to reduced voice spending, with fewer employees directly translating to fewer voice seats needed. While the VoIP product is likely to recover over the longer term, most of the traditional voice customers lost from COVID-19 will be gone forever.

Business Internet (dedicated internet access and standard broadband)

While home internet is surging, business internet is getting hammered by SMB closures and is not seeing any traffic boost from COVID-19. We project traffic will recover somewhat by 2024, but with potentially 20 million workers staying home post-pandemic, it will be a relatively slow recovery. The impact of this on business internet purchasing, however, will be less direct as internet access is not purchased on a “per employee” basis, and businesses are likely to continue purchasing similar levels of internet access despite lower usage so long as they remain in business.

An additional offsetting factor will be the role that business internet often plays in enabling remote work. While remote work’s impact on networking is covered in our forecast separately, in certain cases, businesses may also need to upgrade their internet plans to support greater reliance on services like VPN, which will create some upside for business internet providers.

Networking (VPN and enterprise WAN)

With a record number of Americans working from home, it’s no surprise businesses will be increasing their spend on VPN services relative to 2019 (in addition to potentially upgrading their internet connection to support these services, as noted above). Networking is also less vulnerable to business closures since the providers’ customer base skews toward mid-market and enterprise firms. Overall, we project networking will have a strong post-COVID-19 growth rate through 2024.

Wireless Infrastructure/Wholesale

Since wholesale customers trend bigger (e.g. large carriers), the short-term impact of COVID-19 will be less pronounced. Some wholesale segments, like carrier transport, tower backhaul, and IP transit, will get an immediate boost due to increased traffic. While there are some concerns that small cell fronthaul upgrades will be delayed or shifted due to the pandemic, the impact is likely to be short-lived, and the wholesale segment overall is poised for some positive impact from COVID-19.

Cloud (IaaS)

The cloud (IaaS) market is increasingly intertwined with the B2B wireline market: many large B2B wireline providers increasingly enable their customers’ access to the cloud (e.g., providing enterprises with direct connectivity to cloud data centers) or even begin offering cloud services themselves. This cloud market faces mixed impact from COVID-19. On one hand, cloud providers focused on SMB may face headwinds due to business closures and fewer employees at business locations. But many mid-market and enterprise companies will see their spend surge as more applications migrate to the cloud to enable digital work. Greater adoption of SaaS applications like Zoom and SharePoint will also positively impact the IaaS segment, as many of those SaaS providers spend money on cloud themselves, spurring IaaS demand. As a result, many cloud providers may see revenues from their largest accounts surge, more than offsetting reduced spend from smaller clients due to budget cuts or churn related to business closures and layoffs. That said, the overall outlook for cloud is still positive despite COVID-19, and we see cloud benefiting from additional tailwinds over the long run.

Post-Pandemic

Our analysis shows that providers with greater exposure to SMB – particularly those over-indexed to selling voice, with internet and networking being more insulated – will be more impacted than those that focus more on enterprise. Moving forward, providers focused on wholesale segments and those with direct exposure to enterprise cloud services and applications may see a positive impact from the greater demand and evolution of consumer communication habits resulting from COVID-19. How it unfolds over the long term is harder to predict, but we could see a scenario where telecom and cloud emerge more resilient over the long run with a redistributed workforce, stronger supply chains, and more digitized customer base.

Altman Solon is the largest global strategy consulting firm exclusively working in the TMT sectors, with a cloud consulting focus area.

Research conducted by Altman Vilandrie & Company in June 2020.